Auto Detailing Liability Insurance

One of the most important aspects of running any kind of business is having the right business insurance coverage. Auto Detailing Liability Insurance is no less important.

At an auto detailing shop, your insurance requirements are more specific than many other businesses. This is due to the fact that you have higher potential liabilities while you are working on your customer vehicles. As a result, you also need a more specific version of liability insurance called Garage Keepers Liability Insurance.

What is Garage Keepers Liability Insurance?

General liability insurance alone won’t cut it, you need garage keepers liability to cover the vehicle while in your care, custody, and control. You can learn more in this article on our website about it and you should also discuss it with your insurance agent.

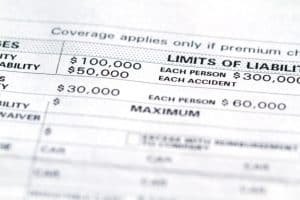

What is Proof of Insurance?

As a business owner, you have an obligation to protect both you and your customers with insurance coverage on your business. When you have the insurance, prove it to your customers. A certificate of insurance aka proof of insurance is the best way to do that. The certificate details exactly what your coverage includes and how it pertains to the services you are performing.

Reputable detail shops will have one right in their office that they can copy, fax, or email to you. Many of our customers will simply ask us to fax them a copy before they bring their car down for service.

Why Do Customers Ask for a Certificate of Insurance?

- Regardless of what kind of vehicle you have, you want to make sure it’s protected while under the care, custody, and control of the shop and it’s employees;

- If you have a more expensive vehicle you want to make sure their coverage exceeds the value of your car. For example, a $90,000 BMW owner would want to look for at least $100,000 in “Garage Keepers Liability Coverage”. This means that the shop is covered regardless if they drive your car into a wall or the shop burns down while your car is in it;

- General Liability will not cover your car! This is important. A lot of shops will try and get around having Garage Keepers Liability while simply carrying General Liability and telling their customers they are fully insured. They are not. General Liability covers your painter if he drops his ladder through your stained glass window, but he’s not in control of your house when he does that damage. Garage Keepers Liability covers the shop while they are in the care, custody, and control of your vehicle. There’s an important difference. Most reputable shops carry both General and Garage Keepers Liability.

- You want to call the insurance agent that is listed on the certificate and make sure to check on auto detailing liability insurance and garage keepers liability insurance coverage. Also, verify that the policy coverage will be in force when you bring your car down to the shop. They will usually verify this for you over the phone. You can also ask them how long they’ve had the policy and whether or not they’ve had any claims. Sometimes the agent will tell you and sometimes they won’t. They will at least tell you whether or not the policy is current, active, and in force.

Care, Custody, and Control

So why is auto detailing liability insurance so important from a shop owner perspective? Here are some things you may not have thought of. Did you know that while your customer’s vehicle is in your care, custody, and control (the three C’s), you are liable for their vehicle?

Don’t Use Personal Auto Insurance for Business

Small businesses are frequently caught committing fraud. Many times without knowing it. They soon find out that ignorance is never a defense when it comes to breaking the law.

How are these businesses committing fraud? One way is by using personal auto insurance as the business auto insurance coverage. As ridiculous as this sounds, it happens often.

Get caught and you’re screwed. Especially if you lie to an insurance agent, claims adjuster, police officer, or customer about having the proper insurance. This has the potential to land you in court or possibly even jail. It’s a big deal, so get the right insurance coverage and don’t play games with your future.

It Can Happen to You

The first thing shop owners tell me when it comes to insurance coverage is, “I’ve never messed anything up, never had a claim, never had a problem.” Same old story, different day. So you don’t think it can happen to you? Think again! I tell people they just jinxed themselves by telling me that. Here are some of the things that have happened at my shops and mobile rigs over the years:

- Burned the paint off a car with a high-speed buffer. One of my detailers went straight to the metal thinking it was “dirt” he was buffing off.

- Ruined all the carpets in a Mercedes after leaving them too wet by forgetting to extract the water from the carpets after cleaning.

- Accidentally etched a windshield with acidic cleaner. This happened several times until we finally switched to a non-etching cleaner because the windshields were costing us so much money.

- Backed a car into another customer car. Inside our shop. Yes, it happened. Several times.

- Drove a Limo through our giant shop garage door. This happened in both forward and reverse, with the same guy stuck between seats cleaning each time. I moved him to our industrial pressure washing team where he wasn’t driving anything. And he became one of my most loyal employees.

These are just a few examples of the many “accidents” that have all happened over the years. It just goes with the territory when you have a booming business with lots of employees. The courts and insurance carriers don’t care if you “didn’t know.” You are expected to know these things if you are in business.

Nothing Good Comes From Lies

So get proper insurance coverage for your business. Start with Auto Detailing Liability Insurance and then go from there. It’s not the only insurance you need to be in business, but it’s a great start.

And never lie. I don’t mean that from a morality basis. It’s just bad for business. Nothing good comes from lies. A customer will catch you and put the word out about you and your business. Trust is almost impossible to earn back after you’ve been caught in a lie. Insurance carriers will drop you, or worse. Other businesses with blackball you. I’ve seen what happens to detailers that lie to dealerships and get caught. You don’t want this to be you. So just be honest.

And you need to set an example in your business. We had a zero-tolerance policy at our shops. Our guys knew the rule, “you lie, you’re out”. Simple.

1099 Contractors or Cash Workers?

When it comes to insurance, another important aspect to think about is the classification of your employees. Are you a business with 1099 contractors or cash workers? If you are, you need to think carefully about how you classify your workers.

Am I passing judgment? Probably. We never had this situation in my businesses. When we were growing fast, there were a few times I had to borrow money from my personal savings to cover payroll, employment taxes, etc. Just workers comp alone will kill many small businesses. I get it. I even missed a few quarterly tax payments when we had several bad months in a row. Getting caught-up nearly killed my business. So I’m telling you from experience. I get what you are going through.

Pass The IRS Criteria to be Considered a Business

Taxes are an unfortunate part of any business. Just keep up with them and everything will go smoother for you.

Paying workers by check as a 1099 independent contractor is inappropriate unless they have their own business. They need to pass specific IRS criteria to be considered a business. Essentially, that means you hire them to do a job, then you leave them to do it. They don’t use your equipment or listen to you tell them how to do their job.

And the most important item? They must have their own insurance. At a minimum, your contractor needs their own liability insurance. All businesses should have this. It’s just good business.

Other insurance coverage depends on the services you offer and the state where your business is located. For example, depending on your state, the contractor might also need to provide you with a proof of coverage certificate for workers’ compensation insurance.

What is Workers’ Compensation Insurance?

Worker’s compensation coverage, also known as worker’s comp, is a type of business insurance that provides benefits to employees that suffer work-related injury or illness. In most states, workers’ comp is: 1) mandatory for employers; 2) replaces 66 2/3% of employee wages; 3) includes payment of medical costs associated with their work-related injury or illness. These benefits are provided to all employees covered under the policy, in exchange for giving up their rights to sue the employer for negligence.

Your state might also allow exemptions from coverage for workers’ comp coverage. Usually, this is only available to the owners or executives of a business. So you definitely need to discuss this with your insurance broker, lawyer, and accountant.

Limit Your Direction or Control of Contractors

This is important in any relationship with your 1099 independent contractors. The directions and control you exert over them must be limited. You hire them for a project, they complete it, give you an invoice and you pay it. Any additional direction or control by you could have them reclassified as W2 employees.

You’re not being smart and getting away with anything. If you get audited, the IRS will notify other government agencies like your state Departments of Revenue and Labor & Industry. You could eventually be responsible for many years of back taxes for both your business and the employee.

that you assumed thought you were getting away with. Try firing a “1099 worker” who then goes to file unemployment because they don’t understand what a 1099 contractor is. The next call you receive might be from a representative of the government just asking a few questions. That’s all it takes to trigger an investigation of you and your business.

Cash and Under the Table Workers

An old friend of mine used to boast about paying all his workers under the table at his construction company. He used all the different methods. Cash payments, 1099 checks, he tried everything. From what he boasted about, this went on for quite some time. He would just laugh at everyone else for paying out taxes. Then he got nailed in an audit because several of his independent contractors filed for unemployment. The department of labor started investigating. They notified the state department of revenue and the IRS. It was a mess. And it cost him dearly.

Don’t be stupid. Follow the rules. And don’t lie. Three simple rules to follow that will help in all aspects of your life. I’m no fan of taxes, but you have to pay them, or eventually, people in suits will show up at your business and take them from you.

Your Insurance Will Not Cover 1099 Contractors

We cover this in more detail on our Detail Shop 1099 Contractor page. I’ve also written a few posts on the subject. As far as your business insurance is concerned, 1099 independent contractors are not employees. So your business insurance will not cover 1099 contractors that are working for you. They are supposed to have their own insurance coverage. It’s actually one of the criteria necessary to prove that they are, in fact, actual businesses.

I won’t even mention cash workers because, well, it’s stupid. Your insurance won’t cover an accident if your ‘contractor’ is involved. Even if you lie and say they are an employee. The insurance adjuster is going to have your $10 or $15 an hour employee state, under oath and penalty of jail time for insurance fraud, that they are an employee. The adjuster might even demand payroll records if they are suspicious of their status as an employee.

You will get caught. I’ve seen shop owners that I’m still friends with that were forced to shut down their businesses because they got nailed with penalties and fines for getting caught doing this.

Garage Keepers Liability Insurance with Transporter Plates

Insurance is also tough when transporting cars. In Pennsylvania, they have special plates called “Transporter” plates. Auctions use these plates to transport cars between auctions and dealers. Detail shops use them for the same thing, except they aren’t really designed for that.

The only way you can get “transporter” plates is to convince a dealership to do a contract with you that says you will be transporting cars for them. The application specifically says that you can’t be driving their cars between your shop and the dealership. So basically they don’t want detailers moving cars and this is their way of making it hard on them. You need garage keepers liability insurance with transporter plates since you will be housing the cars when you transport them to your shop. Even though technically the plates aren’t designed for that use. We cover this in more detail on our Detail Shop Transporter Plate page. Our shop got around this by just getting repair/towing plates since we were doing auto reconditioning services on cars. It worked out and allowed us to stay in compliance with the law. Check out the transporter plate page for more info on this.

Get Proper Insurance Coverage

The detailing business is like any other when it comes to being properly insured. The reason you have auto detailing liability insurance is to make sure you are covered in the event something bad happens. So by cutting corners like many detail shop owners do, eventually you will get burned in some scenario that you might have thought sounded good but in reality just doesn’t work.

Just do the right thing and get the proper insurance coverage with good auto detailing liability insurance and garage keepers liability insurance if needed. The nice thing about the garage keepers insurance is that most policies cover both the physical damage part of your activities and also the other liability issues that you need coverage for in your business.

Liability insurance is one of the most important types of insurance you can obtain for your business. So get it. You will be glad you did.